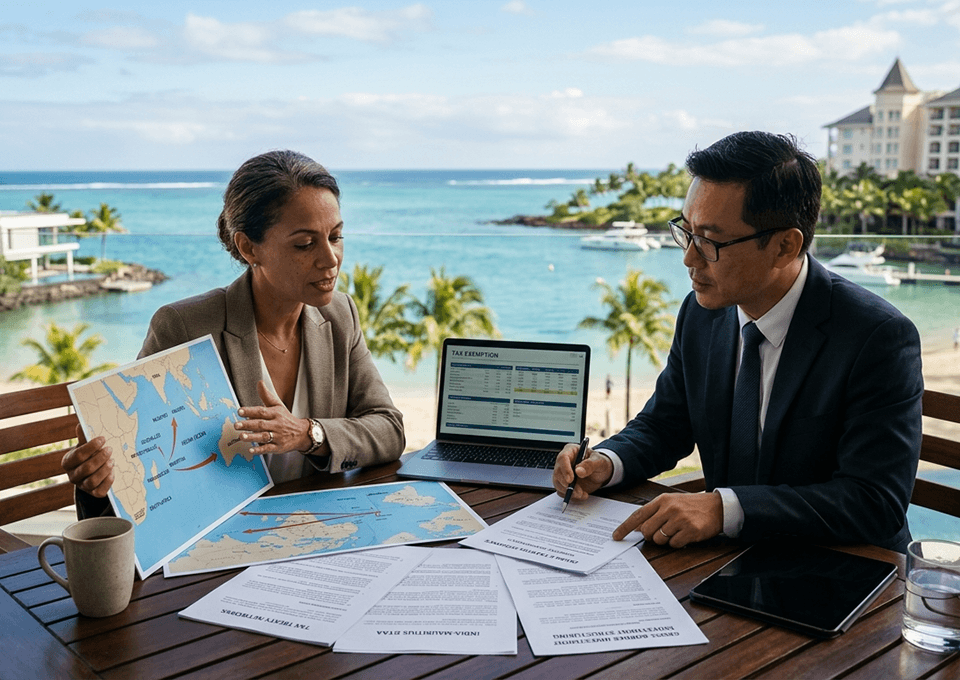

For investors considering real estate investment across multiple Indian Ocean jurisdictions, or for international investors using Mauritius as a platform to access broader investment opportunities in Africa, Asia, and the region, the tax treaty framework of the relevant jurisdictions is among the most important but most frequently underweighted analytical inputs in the investment decision and structuring process. Tax treaties determine how income and capital gains are taxed as they flow across national borders, prevent the double taxation that would otherwise make cross-border investment economically unattractive at scale, and create the tax efficiency that enables international capital to be mobilised and deployed at the volumes that generate genuine economic development.

Mauritius has built one of the most extensive, carefully maintained, and internationally respected treaty networks in the Indian Ocean region, with bilateral tax treaties covering a substantial number of jurisdictions across Africa, Asia, Europe, and beyond. This treaty network is one of the structural factors that has made Mauritius an attractive platform for international investors, not just in real estate but across asset classes. Understanding how the Mauritius treaty network actually works in practice, and what it means concretely for real estate investment decisions by buyers and investors in developments including those of the Apavou Group, is essential knowledge for any serious cross-border investor in the region.

How Tax Treaties Work, The Core Mechanics

A bilateral tax treaty between two countries establishes agreed rules for how different categories of income and capital gains generated by residents of one country from activities or investments in the other country will be taxed. Without a treaty, income or gains generated in a foreign country may be subject to tax in both the source country where the income arises and in the residence country where the investor is tax resident, creating double taxation that substantially reduces net investment returns and creates significant administrative complexity.

Tax treaties prevent this double taxation by allocating taxing rights between the two contracting states, typically by limiting withholding tax rates on cross-border dividends, interest, and royalties to agreed reduced rates, by determining in which country capital gains on specific asset categories will be taxed, and by providing relief mechanisms (either exemption or tax credit) for taxes paid in the source country against the residence country tax liability. For real estate investment specifically, the most relevant treaty provisions address the treatment of rental income from immovable property, capital gains arising on the disposal of property assets, and the taxation of income from vehicles that hold real estate assets.

The Mauritius Treaty Network, Its Scope and Strategic Significance

Mauritius has bilateral tax treaties with over forty countries, including many of the most significant sources of international investment capital relevant to the Indian Ocean real estate market, France, the United Kingdom, Germany, South Africa, India, Singapore, China, Japan, and others. This extensive and well-maintained treaty network makes Mauritius one of the most attractive and legally sophisticated platforms in the region for structuring cross-border investments that benefit from treaty protections.

For international investors acquiring real estate in Mauritius, or using a Mauritius platform to invest elsewhere in the region, the treaty network provides meaningful clarity on the tax treatment of investment returns, significantly reduces the regulatory uncertainty that non-treaty situations create, and enables more accurate projection of after-tax investment returns in financial models. The Mauritius Global Business Company structure, a specific vehicle developed under the island’s financial services regulatory framework, is widely used by international investors to access treaty benefits in the context of both real estate and financial investments across the region.

How Treaty Benefits Are Accessed in Practice for Mauritius Real Estate

For an international investor acquiring a property in Mauritius through an IRS or PDS scheme, such as a residential development by the Apavou Group or a comparable established developer, the practical treaty planning question is whether and how Mauritius’s treaty network interacts with the investor’s home jurisdiction tax obligations on the rental income and eventual capital gains generated by the Mauritius investment. The answer is always specific to the investor’s particular circumstances, their country of tax residence, the specific nature of their Mauritius holding structure, their overall investment portfolio, and their longer-term intentions regarding the property. Qualified professional advice from practitioners expert in both Mauritius tax law and the investor’s home jurisdiction tax law is essential to optimising this cross-border tax position accurately.

The Mauritius Treaty Network and Real Estate Development Investment

For institutional and professional investors considering equity or debt investment in major Mauritius real estate development projects, including large-scale commercial and mixed-use developments of the kind that the Apavou Group has historically delivered through Plaisance Mall, The Cube, and Terre d’Été, the Mauritius treaty network provides a stable and sophisticated legal framework for structuring those investment relationships in a tax-efficient manner.

Development joint ventures, project finance structures, and co-investment arrangements between Mauritius-based developers and international capital providers can be structured through Mauritius entities in ways that access treaty protections for cross-border income flows, provide a stable and internationally recognised legal framework for the investment relationship, and facilitate the repatriation of investment returns and principal in a manner that is transparent, legally predictable, and tax-efficient for all parties. The sophistication of the Mauritius financial services regulatory framework, including the infrastructure of qualified lawyers, accountants, fund administrators, and corporate services providers that has developed around the Mauritius Global Business sector, supports the implementation of these structures at a professional standard that commands international confidence.

Substance Requirements, The Evolving Standard for Treaty Access

In response to international anti-avoidance initiatives, particularly the OECD’s Base Erosion and Profit Shifting project and the associated Multilateral Instrument, Mauritius has progressively strengthened the economic substance requirements that must be met by entities claiming treaty benefits. A Mauritius company or global business entity claiming treaty protections must now demonstrate genuine economic presence in Mauritius, real management and control functions being exercised locally, qualified employees working in Mauritius, adequate local operational expenditure, rather than simply being incorporated in Mauritius through a nominee arrangement as was historically possible.

These substance requirements add to the cost and administrative complexity of using Mauritius treaty structures, and investors must carefully assess whether the treaty benefits available in their specific circumstances justify the substance maintenance costs for their investment size and structure. For larger investments, including significant real estate development exposures in the Mauritius market, the benefits of treaty-efficient structuring typically outweigh the costs of substance compliance substantially. For smaller investments, simpler direct ownership structures without formal treaty planning may represent a more appropriate balance of cost and benefit.

Treaty Frameworks Across Other Indian Ocean Jurisdictions

Mauritius has the most extensive and sophisticated treaty network of any Indian Ocean island jurisdiction, a leadership position that reflects the deliberate and sustained investment the island has made in building its financial services and international investment infrastructure over decades. Other jurisdictions in the region have treaty relationships of varying scope and sophistication. Seychelles has expanded its treaty network significantly in recent years as part of its effort to develop a comparable financial services sector. La Réunion, as an integral part of France, benefits from the French treaty network, one of the most extensive in the world, making it attractive for French-resident investors with specific treaty requirements. Madagascar, Comoros, and other regional jurisdictions have more limited treaty coverage that creates real constraints on tax-efficient cross-border investment structuring.

Investors considering exposure across multiple Indian Ocean jurisdictions should evaluate the treaty position of each jurisdiction relative to their specific investor profile and home country tax residence, rather than assuming that the Mauritius framework is universally optimal for all cross-border investment scenarios in the region. The right structuring answer depends on the investor’s residence, the specific target jurisdictions for investment, the nature of the investment, and the specific treaty provisions applicable to the relevant income and gain categories.

Tax Efficiency as a Material Component of Investment Return

In cross-border real estate investment in the Indian Ocean region, the tax treatment of investment returns is not a technical afterthought to be addressed after the commercial investment decision is made. It is a material component of total after-tax return that must be analysed and optimised as an integral part of the investment decision-making process. Mauritius’s extensive treaty network, its well-established and internationally recognised financial services infrastructure, its stable and transparent regulatory environment, and its proactive approach to meeting international standards of substance and transparency make it one of the most effective and credible platforms for cross-border investment structuring in the region. For serious investors in the Indian Ocean real estate space, including those considering investments in landmark Mauritius developments, understanding and appropriately utilising these tax efficiency advantages is an important dimension of investment performance that should not be left to chance.

Previous Post

Previous Post Next Post

Next Post